Key Takeaways

- Rising home prices, stagnant wages, and limited housing inventory are creating a significant affordability squeeze, making homeownership increasingly out of reach for many Americans.

- This crisis disproportionately affects first-time homebuyers, low- and middle-income families, and renters, impacting economic growth, social mobility, and overall well-being.

- The consequences extend beyond financial strain, leading to increased housing insecurity, social mobility stagnation, and negative mental and physical health effects.

- Potential solutions include increasing housing supply, supporting first-time homebuyers, regulating the rental market, exploring community land trusts, and long-term government investment.

- Addressing this issue requires a multi-pronged approach to ensure a more equitable and accessible housing market for all.

Homeownership has long been a cornerstone of the American Dream. It represents stability, financial security, and a place to build a life. However, the recent decline in housing affordability threatens to push this dream further out of reach for millions of Americans.

This article from Brickfront Properties LLC and Local Washington DC Construction delves into the factors contributing to this decline, explores its widespread impact, and discusses potential solutions to get the housing market back on track.

Understanding the Affordability Squeeze

A confluence of factors is driving the decline in housing affordability. Here’s a breakdown of the key culprits:

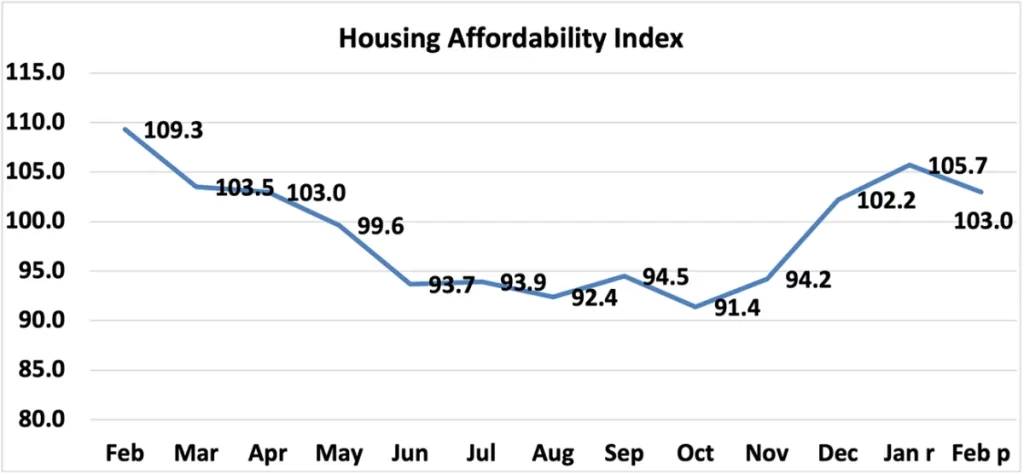

- Rising Home Prices: Fueled by low interest rates and a shortage of available homes, housing prices have skyrocketed in recent years. This surge in price outpaces wage growth, making it increasingly difficult for potential buyers to save for a down payment and qualify for a mortgage.

- Rising Interest Rates: In an attempt to combat inflation, the Federal Reserve has raised interest rates. While this might cool down the housing market, it also translates to higher borrowing costs for mortgages. This monthly burden further strains affordability for many aspiring homeowners.

- Limited Housing Inventory: The ongoing supply-demand imbalance remains a critical issue. New home construction hasn’t kept pace with population growth, creating a shortage of available homes on the market. This limited inventory allows sellers to command higher prices, further pushing affordability out of reach.

The Ripple Effect: Who Feels the Squeeze?

The decline in housing affordability isn’t a singular problem. It has a cascading effect across various demographics and the economy as a whole. Let’s explore some of the most impacted groups:

- First-Time Homebuyers: Millennials and Gen Z face the brunt of the affordability crisis. This generation entered the housing market burdened with student loan debt and stagnant wages. Soaring home prices and rising interest rates make homeownership a distant dream for many.

- Low- and Middle-Income Families: As affordability shrinks, low- and middle-income families struggle to find decent, secure housing within their budget. This often leads to overcrowding, increased competition for rentals, and a strain on already stretched finances.

- The Rental Market: The ripple effect doesn’t stop there. As potential homebuyers are priced out of the market, they turn to rentals, increasing demand and driving up rental prices. This creates a domino effect, impacting renters across the income spectrum.

- The Economy: A stagnant housing market can hinder economic growth. When a significant portion of the population struggles to afford a home, it can lead to decreased consumer spending, impacting various industries and slowing down economic activity.

Beyond the Numbers: The Human Cost of Affordability

The impact of housing affordability goes beyond financial strain. It has a direct effect on the well-being of individuals and communities:

- Increased Housing Insecurity: Rising housing costs lead to increased housing insecurity, which is the state of living in an unstable or inadequate housing situation. This can lead to homelessness, frequent moves, and a sense of instability, particularly for low-income families.

- Social Mobility Stagnation: Homeownership has traditionally been a vehicle for wealth creation and social mobility. When the dream of homeownership becomes unattainable, it creates a cycle of intergenerational poverty, hindering opportunities for upward mobility.

- Mental and Physical Health Impacts: Housing insecurity has a demonstrably negative impact on mental and physical health. The stress of unstable housing situations can lead to anxiety, depression, and chronic health issues.

Potential Solutions: A Path Forward

Addressing the housing affordability crisis requires a multi-pronged approach. Here are some potential solutions:

- Increase Housing Supply: Incentivizing the construction of new homes, particularly affordable housing units, is crucial to address the supply shortage. Streamlining zoning regulations and providing tax breaks for developers building affordable housing can create a more favorable environment for increased supply.

- Support for First-Time Homebuyers: Policies supporting first-time homebuyers, such as down payment assistance programs and tax credits, can ease the financial burden of entering the market.

- Rental Market Regulations: Implementing rent stabilization measures and tenant protections can help curb rising rental prices and ensure greater stability for renters.

- Community Land Trusts: Community land trusts (CLTs) are non-profit organizations that own the land under a property while individuals own the structure. This model can provide a pathway to homeownership for low- and moderate-income families.

- Long-Term Investment: Government investment in affordable housing initiatives, coupled with public-private partnerships, can provide the resources needed to create and maintain a sustainable stock of affordable housing.

Conclusion: Building a More Equitable Housing Market

The decline in housing affordability is a pressing issue demanding immediate and effective solutions. By implementing the strategies outlined above, we can work towards a more equitable housing market. Increasing the supply of affordable homes, providing targeted assistance to those struggling to enter the market, and ensuring stability for renters are all crucial steps.

However, addressing this crisis necessitates a collective effort. Policymakers, developers, community organizations, and individual citizens all have a role to play. Investing in a robust and accessible housing market isn’t just about securing the American Dream for future generations; it’s about fostering strong, stable communities and a thriving economy.

We at Brickfront Properties LLC and Local Washington DC Construction say “Let’s work together to ensure that the dream of a safe and secure place to call home remains a reality for all Americans.”